Operating Leases

Semiconductor Manufacturing Equipment

Operating leases are very effective arrangements for hedging the risk of semiconductor manufacturing equipment, lowering the cost of such equipment, keeping these assets off the balance sheet, and achieving other financial objectives.

Outline of the Transactions

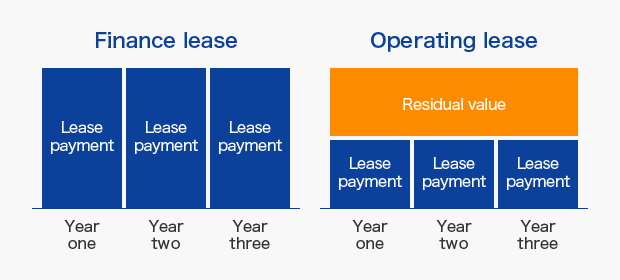

Under operating lease schemes, the leasing company examines the value of the equipment after the expiration of the lease term (residual value), and then subtracts the residual value from the price of the item. The customer then pays the difference as lease fees. Since SMFL takes the risk (in principle) of the future value of the item, customers can receive the benefits of paying substantially lower leasing fees. In addition, by designing the operating lease according to the accounting and tax regulations of Japan and the United States, operating leases can be effective in realizing clients’ financial strategy of keeping items off the balance sheet.

Please enlarge and see.

- In the case of finance leases, lease terms are limited to a minimum of three years, but using operating leases, customers can choose relatively short lease terms and set the terms to meet the needs of R&D, foundry, and other types of projects.

- The customers can select the equipment as in the case of regular purchase.

- Depending on the manufacturer of the equipment, the model, its specifications, timing of introduction, lease period, and other characteristics, SMFL determines the residual value.

- As is the case with finance leases, such operating leases cannot be cancelled before completion of the contract term.

- For maintenance, as with regular purchases, the customers sign maintenance contracts with the respective manufacturers

- After completion of the lease, customers may choose (1) to return the items, (2) re-lease the item (secondary lease), or (3) purchase the item (provided such arrangements have been made).

Features and Advantages

- Risk of obsolescence (technical innovation)

- These leasing arrangements make it possible for manufacturers to introduce the latest equipment in line with their production plans and thereby create efficient production lines.

- Ownership risk (idle assets)

- These arrangements prevent overcapacity in the future and facilitate decision making regarding equipment replacements. Also, when the equipment is expected to have residual value, this reduces the cost.

- Depreciation risk (depreciable assets, removal losses)

- Under these arrangements, customers can avoid having to record accounting losses because of removal losses, and replace their equipment. The effect is the same as making the useful life of the equipment for depreciation purposes the same the period the equipment is actually used.

- Off-balance sheet advantages

- Even after changes in accounting standards, these arrangements provide the benefits of off-balance sheet accounting even under international accounting standards. This provides the benefit of improving credit ratings and contributes to improving the customer’s financial position.

- Increase in free cash flow

- Since these arrangements effectively outsource capital investments, this provides for greater leeway in cash flows and increases flexibility from a financial strategy perspective.